CSL Shares Hit Decade Low Amid Financial Challenges

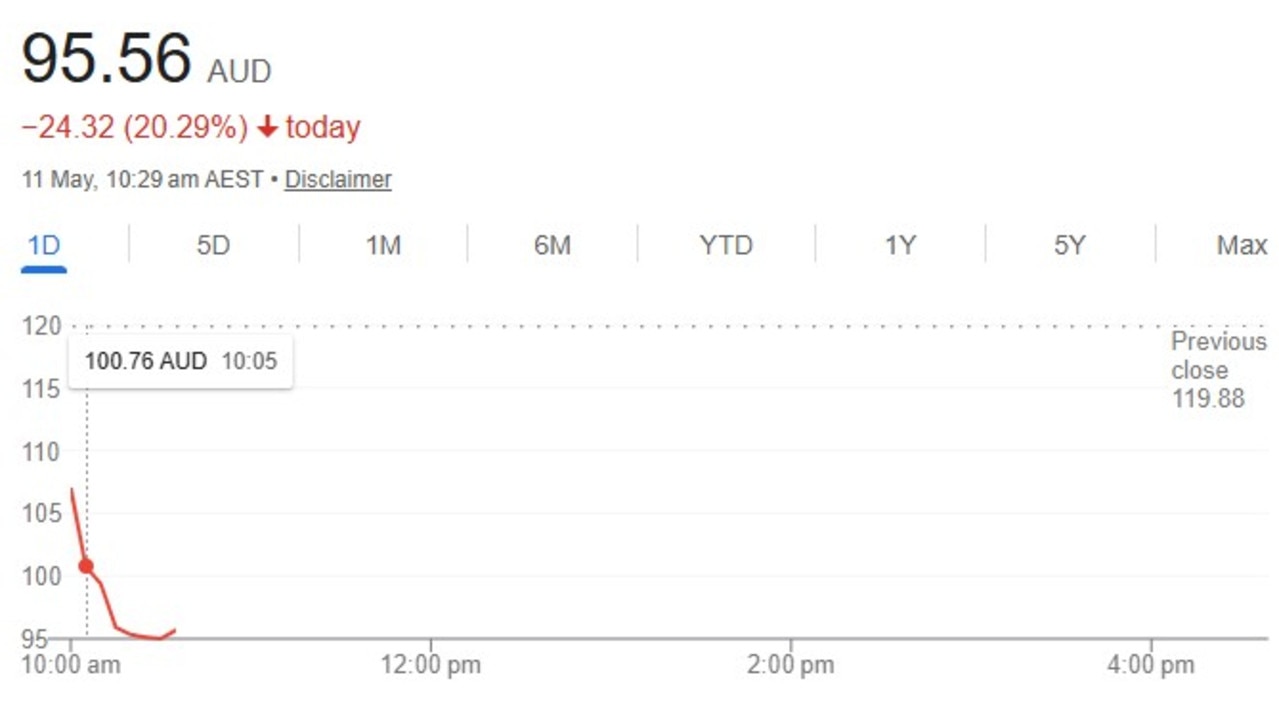

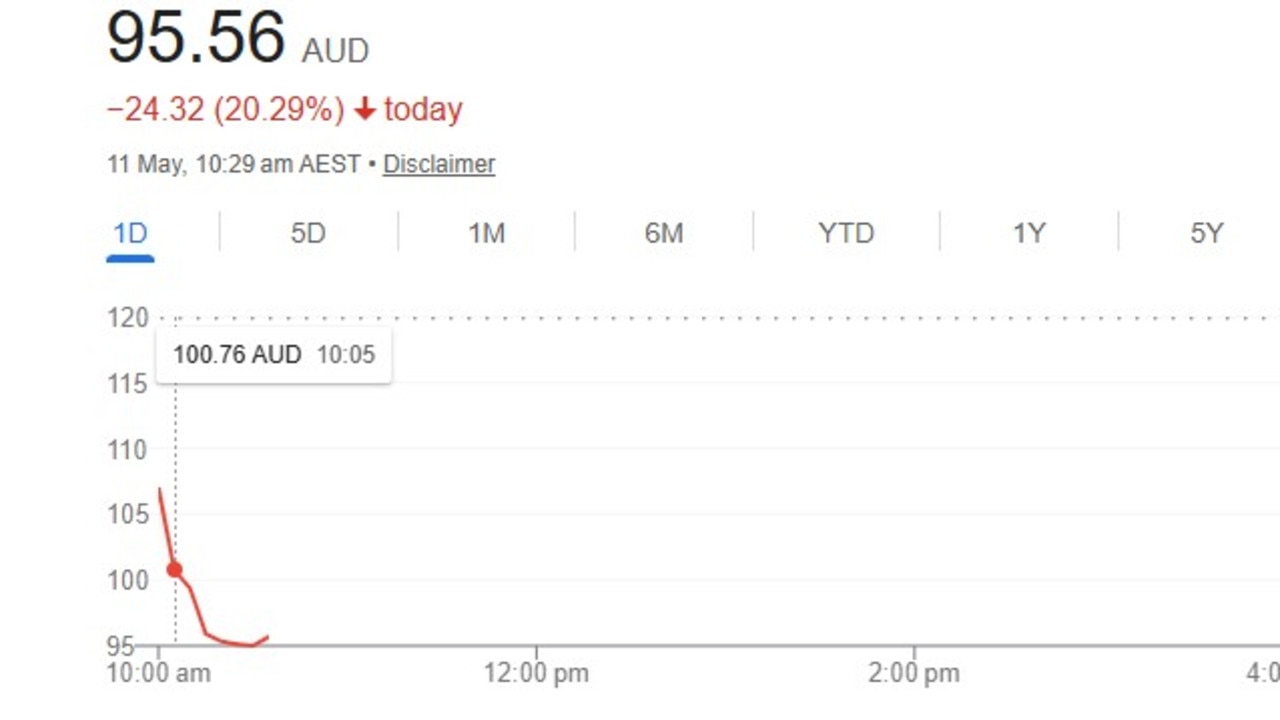

Shares of healthcare giant CSL have experienced a significant drop, falling by 20 per cent to a decade low. This decline follows the company’s announcement of an additional $US5 billion non-cash impairment as part of a 90-day review. The first $1.5 billion of this write-down was already accounted for in the first-half results.

The market reaction has been swift and severe. On the day of the announcement, shares plummeted by 20.29 per cent at the opening, trading below $100 per share for the first time in over a decade. This marks a sharp contrast to the peak during the pandemic when shares reached around $340 per share, driven by high vaccine demand.

The weaker-than-expected performance in overseas markets has contributed to the downturn. Despite these challenges, CSL still anticipates revenue of $US15.1 billion (approximately $A21 billion) and a net profit of $3.1 billion, slightly lower than previous estimates of $3.3 billion.

This revised forecast includes an additional $US300 million write-down for its US immunoglobulin business, along with a $US200 million hit to its albumin business in China. These financial adjustments highlight the ongoing difficulties the company is facing in key markets.

The recent downgrade was announced by CSL’s interim chief executive, Gordon Naylor, who took over the role just three months ago after the abrupt departure of former CEO Paul McKenzie. Mr Naylor acknowledged the challenging results but expressed confidence in the company’s direction.

“Our growth initiatives are working, but the financial benefits will take longer than previously anticipated to materialise,” he stated. “As a result, we have now revised down our 2026 financial year guidance.”

In August, CSL faced another major setback, losing $21 billion in a single day of trading. This followed the announcement of a bold restructuring plan that included cutting 3,000 global roles, which would cost $770 million initially but was expected to save between $500 million and $550 million over three years.

Additionally, CSL revealed plans to demerge its influenza prevention vaccines unit, Seqirus, into a separate ASX-listed business by 2026. The company also intends to combine the commercial and medical operations of its core blood plasma and iron deficiency businesses into one integrated unit.

CSL exports plasma-derived therapies to the United States. In a statement, the company noted that it does not expect any material impact from US tariffs on pharmaceuticals, as lifesaving medicines are likely to be exempt from such measures.