S&P/ASX 200 Surges as Defensive Stocks Lead the Way

The S&P/ASX 200 closed with a significant gain of 99.4 points, marking an increase of 1.17%. This upward movement came after President Trump called off planned military strikes on Iran, which led to a drop in oil prices and stabilized benchmark bond yields. The shift prompted a rotation into defensive stocks, with consumer staples, healthcare, and major banks all performing strongly. In contrast, materials and technology stocks saw less demand.

For those interested in a comprehensive overview of today’s market movements, including sector-specific updates, broker responses, and key economic data, there is a detailed Evening Wrap available. Additionally, the ChartWatch section provides in-depth technical analysis on both the Nasdaq Composite and the S&P/ASX 200.

Today in Review

On Tuesday, 19 May, at 5:12pm (AEST), the following were the closing values for major indices:

- ASX 200: 8,604.7 (+1.17%)

- All Ords: 8,829.5 (+1.08%)

- Small Ords: 3,386.0 (+0.62%)

- All Tech: 2,797.9 (+0.84%)

- Emerging Companies: 2,966.4 (-0.83%)

In terms of currency, the AUD/USD rate was at 0.7134, a decrease of 0.48%.

Looking at US futures:

- S&P 500: 7,412.75 (-0.18%)

- Dow Jones: 49,730.0 (-0.08%)

- Nasdaq: 29,004.5 (-0.31%)

Sector Performance

The performance across different sectors was as follows:

- Consumer Staples: +3.0%

- Communication Services: +2.66%

- Health Care: +1.87%

- Real Estate: +1.81%

- Financials: +1.72%

- Consumer Discretionary: +1.52%

- Industrials: +1.23%

- Utilities: +1.02%

- Energy: +0.52%

- Materials: -0.07%

- Information Technology: -0.43%

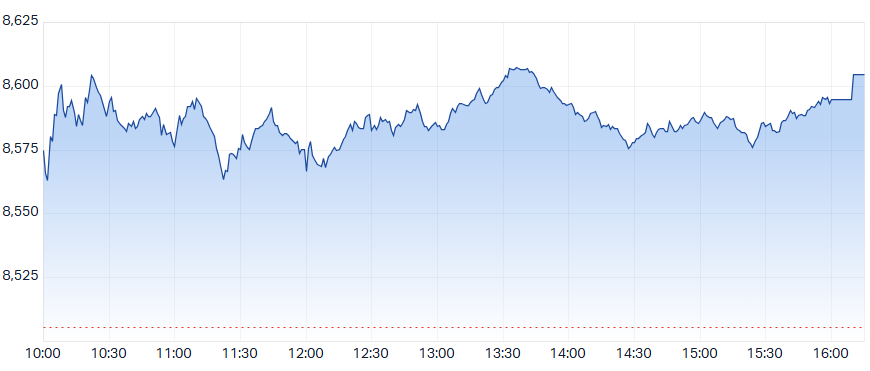

ASX 200 Session Chart

The S&P/ASX 200 (XJO) finished 99.4 points higher at 8,604.7, representing a 1.2% increase from its session low and reaching its session high. In the broader-based S&P/ASX 300 (XKO), advancers outperformed decliners by a margin of 206 to 77 — a significant reversal from the previous day!

Consumer Staples (XSJ) +3.0%

As investors shifted towards defensive stocks, the Consumer Staples sector emerged as the top performer. With the anticipated Wall Street overnight collapse not materializing, fund managers cautiously added risk, focusing on high-quality blue chips while largely ignoring cyclicals. Lower oil prices helped ease cost-of-living pressures, reinforcing the sector’s appeal.

Woolworths (WOW) gained 3.7%, supported by a JPMorgan upgrade to Overweight with a price target lift to $37.00. Treasury Wine Estates (TWE) and Coles (COL) also saw gains, with Metcash (MTS) rising by 2.7%.

Communication Services (XTJ) +2.7%

The Communication Services sector also benefited from the defensive rotation. Blue-chip names within this sector, known for their predictable earnings and reliable dividends, aligned with the theme of adding risk conservatively. CAR Group (CAR), Seek (SEK), and Telstra (TLS) all advanced.

Health Care (XHJ) +1.9%

The Health Care sector had a strong session, consistent with the defensive rotation. Pro Medicus (PME), CSL (CSL), Ramsay Health Care (RHC), and Cochlear (COH) all recovered ground lost earlier in the week.

Real Estate (XPJ) +1.8%

The Real Estate sector was one of the biggest beneficiaries as benchmark bond yields retreated from Monday’s multi-year highs. Goodman Group (GMG) and Stockland (SGP) were among the stronger movers.

Financials (XFJ) +1.7%

The Financials sector also recovered alongside the retreat in bond yields. The big four banks each added more than 1.3%. AMP (AMP) and QBE Insurance (QBE) led as the insurance sector shone.

Consumer Discretionary (XDJ) +1.5%

The Consumer Discretionary sector gained as the modest decline in oil prices eased cost-of-living pressure and lifted consumer sentiment. Domino’s Pizza Enterprises (DMP), Propel Funeral Partners (PFP), and Wesfarmers (WES) were standout performers.

Energy (XEJ) +0.5%

Despite a 1.9% fall in ICE Brent crude futures to US$109.98/bbl, the Energy sector was firmer. Coal stocks surged as global Coal Newcastle coal futures gained 1.2% to $140.45/t. New Hope Corp. (NHC), Yancoal Australia (YAL), and Whitehaven Coal (WHC) were standouts.

Information Technology (XIJ) -0.4%

The Information Technology sector tracked weakness in Nasdaq-listed AI infrastructure stocks on Monday. Technology One (TNE) was the worst performer after a first-half profit miss on foreign currency headwinds.

Key Stock Movements

Best Gainers in the ASX 300

| Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

| Tuas (TUA) | $2.67 | +$0.4 | +17.6% | -55.6% | -53.3% |

| ALS (ALQ) | $23.32 | +$1.49 | +6.8% | +4.2% | +31.7% |

| Tyro Payments (TYR) | $0.760 | +$0.045 | +6.3% | -8.4% | -15.6% |

| G8 Education (GEM) | $0.170 | +$0.01 | +6.3% | -32.0% | -86.7% |

| Ora Banda Mining (OBM) | $1.405 | +$0.08 | +6.0% | -9.9% | +42.6% |

Worst Losers in the ASX 300

| Company | Last Price | Change $ | Change % | 1mo % | 1yr % |

|---|---|---|---|---|---|

| 4DMEDICAL (4DX) | $3.65 | -$0.35 | -8.8% | -35.9% | +1203.6% |

| Predictive Discovery (PDI) | $0.835 | -$0.07 | -7.7% | -12.1% | +116.9% |

| Sunrise Energy Metals (SRL) | $12.19 | -$0.87 | -6.7% | +3.7% | +2076.8% |

| Droneshield (DRO) | $2.94 | -$0.19 | -6.1% | -18.6% | +141.0% |

| Lynas Rare Earths (LYC) | $18.12 | -$0.81 | -4.3% | -11.1% | +139.1% |

ChartWatch Analysis

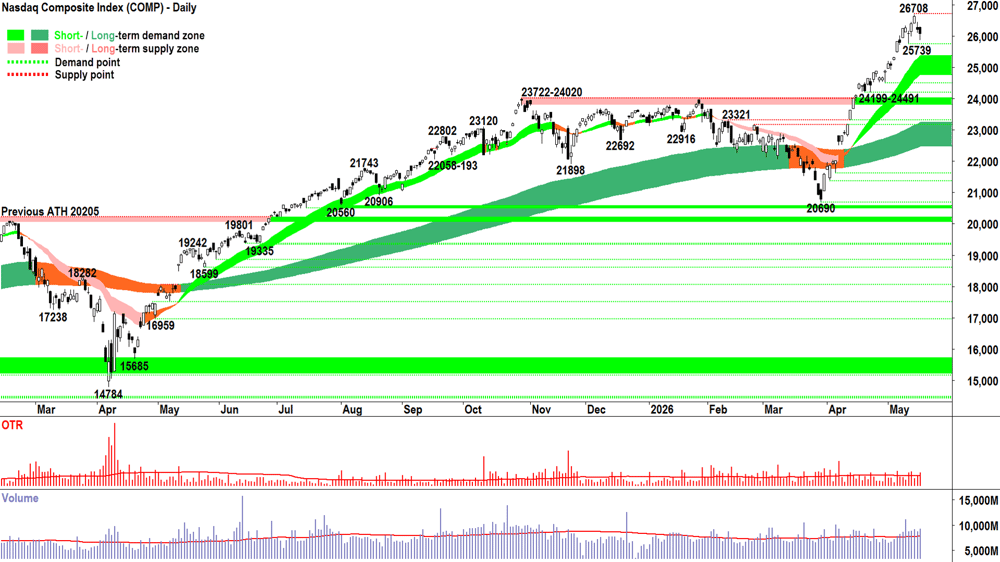

Nasdaq Composite Index

Analysis of the Nasdaq Composite Index suggests that despite initial concerns about the bond market, the index showed resilience. The chart indicates a monster uptrend with a point of supply set. The dip buying occurred near a previous defined point of demand, indicating potential for further growth.

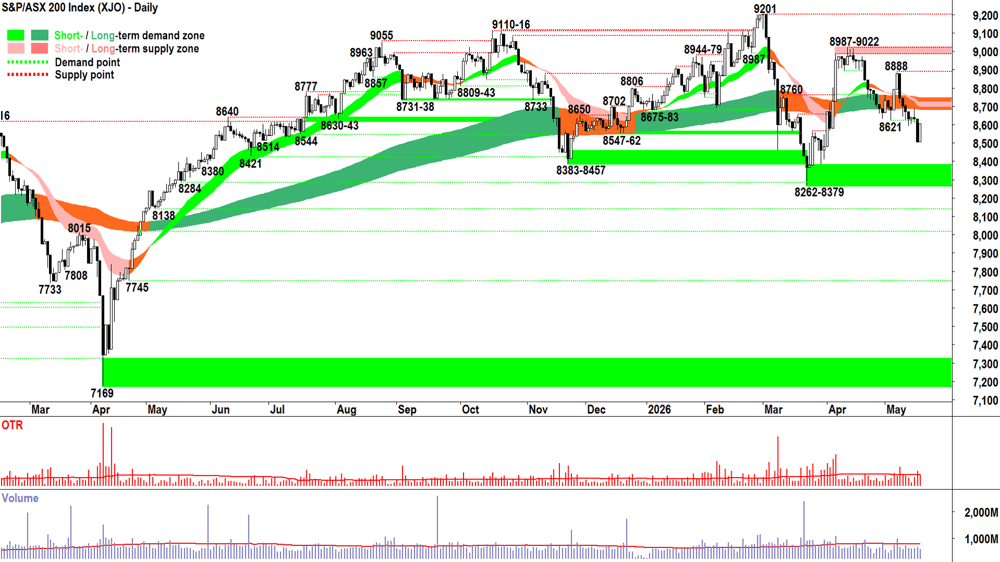

S&P/ASX 200 (XJO)

The S&P/ASX 200 showed signs of recovery, with a candle that reflected sustained excess demand into the close. However, the volume was modest, suggesting limited engagement from both demand and supply sides. The key levels to watch include 26708 as a point of supply and 25739 as a point of demand.

Economy

Today’s economic data included the AUS May Westpac Consumer Sentiment, which rose by 3.5% to 83, showing a rebound from the initial fuel price spike. However, the overall sentiment remained “deeply pessimistic.”

Upcoming Economic Data

- Tuesday: USA April Pending Home Sales (forecast +1.2% m/m)

- Wednesday: CHN Peoples Bank of China (PBOC) Official Interest Rates Decision

- Thursday: US Federal Reserve May FOMC meeting minutes and AUS April Employment Data

- Friday: No major economic data scheduled

Latest News and Technical Analysis

Several companies, including CSL, Brambles, Ansell, Charter Hall, Endeavour Group, James Hardie, Stockland, and Sonic Healthcare, were highlighted in the latest technical analysis.

Market Wraps

Various market wraps provided insights into the ASX 200, A2M, AGL, and other key stocks. The evening wrap noted a slump in the ASX 200 due to a spike in global bond yields, which triggered a major reset for gold and mining stocks.

Broker Moves

Numerous broker moves were reported, with several companies retaining or upgrading their ratings. For example, ALS Limited (ALQ) received multiple buy ratings, while Alcidion Group (ALC) was retained at buy at Bell Potter.

Interesting Movers

Notable stock movements included Northern Minerals (NTU) gaining 21.7% and Tuas (TUA) rising 17.6%. On the flip side, 4DMedical (4DX) fell by 8.8%.

Want Free Investment Tools?

Market Index offers investors access to broker consensus, ASX announcement data, dividend information, and much more. Click here to access everything 100% free.