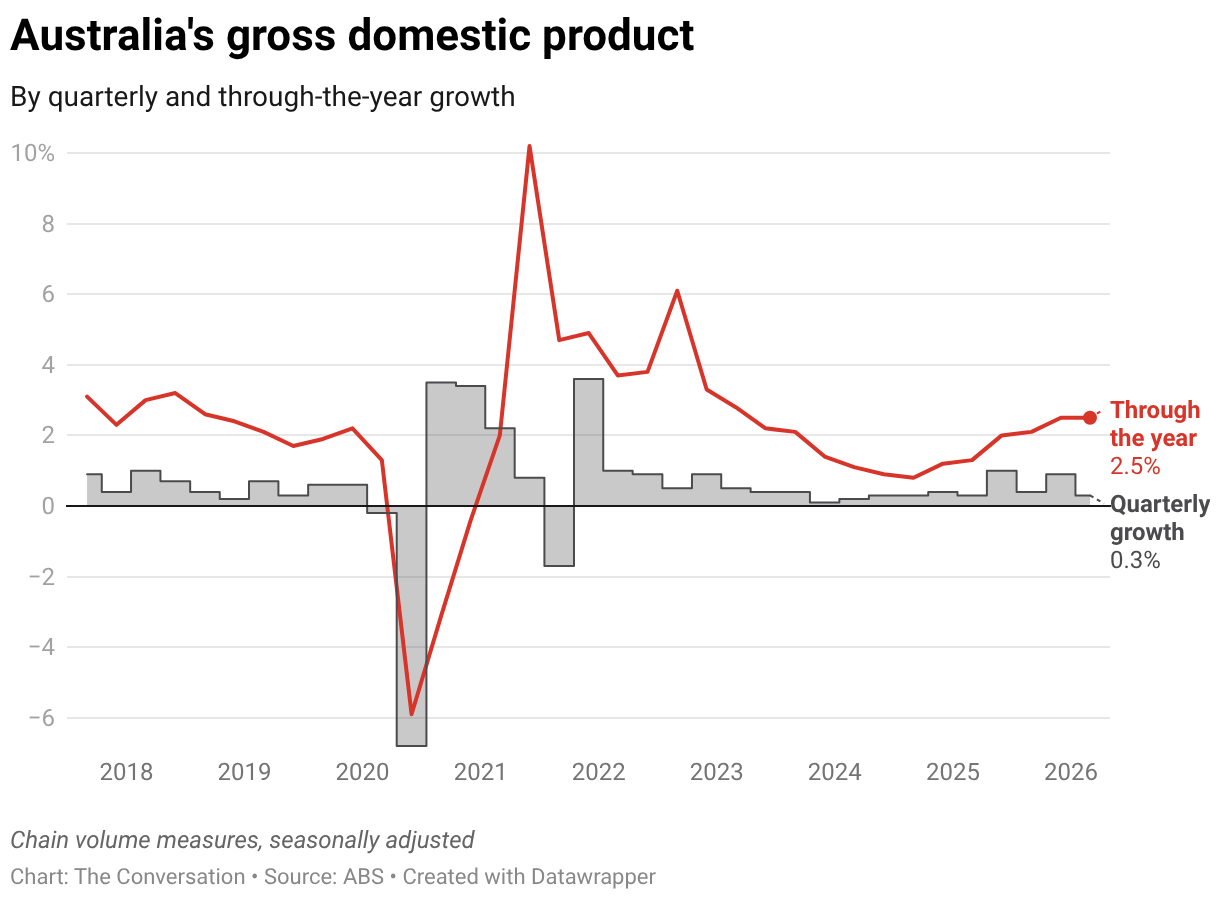

Australia’s economy experienced a slower growth rate in the first quarter of 2026, expanding by 0.3% compared to the previous quarter’s 0.9% growth. According to data from the Australian Bureau of Statistics (ABS), the annual GDP growth for the year ending March 2026 was 2.5%. However, when adjusted for population growth, GDP per person actually declined by 0.1% in the quarter. This indicates that while the overall economy is still growing, the average Australian may not be feeling significantly better off.

The slowdown in economic growth has raised questions about the future direction of interest rates. The Reserve Bank of Australia is expected to consider maintaining current rates at its June meeting, following recent increases in February, March, and May. Although inflation remains a concern, the latest figures suggest that previous rate hikes have already started to impact household spending and economic activity.

Impact of Higher Fuel Prices

The ongoing conflict in the Middle East, which began on February 28, has had a direct effect on Australia’s economy through rising fuel and fertiliser prices. The ABS reported a sharp increase in automotive fuel prices towards the end of the March quarter. However, the federal government’s fuel discounts only took effect in April, leaving households to deal with higher costs during the quarter.

As a result, many Australians have shifted their spending habits, prioritising essentials over discretionary purchases. Discretionary spending remained weak, indicating a cautious approach among consumers. Spending on electricity, gas, and other fuels also increased sharply after energy rebates ended, while vehicle operating costs rose due to concerns about petrol and diesel supplies.

Sectors Driving Growth

Despite the overall slowdown, certain parts of the economy showed strong performance. Private investment was the most significant contributor to growth, driven by a surge in machinery and equipment investment. This increase was largely attributed to business investments in data centres located in New South Wales and Victoria. This trend highlights a broader shift towards digital infrastructure and artificial intelligence, even amid economic challenges.

The GDP figures reveal a growing divide within the Australian economy. Sectors such as data centres, engineering services, IT consulting, and construction are experiencing rapid expansion, while many consumer-facing industries continue to face pressure. Household consumption did grow, but the increase was primarily concentrated in essential goods rather than discretionary spending. This pattern suggests that households are spending more on necessities due to rising costs or concerns about supply chain shortages.

Industries Facing Decline

Net trade was the main factor dragging down economic growth. Exports fell while imports rose, with the decline in exports attributed to disruptions in coal and iron ore production caused by bad weather. Imports increased partly due to record levels of automatic data processing equipment, linked to the growth in data centre investment.

Government spending also decreased, partly because of the end of energy bill relief. The mining sector saw the largest industry decline, with coal production affected by Cyclone Koji. Consumer-facing services, including retail trade, accommodation, and food services, remained weak, reflecting subdued discretionary spending.

Watching for a Per Person Recession

A key question is whether this slowdown is temporary or the beginning of a more significant economic downturn. While the overall economy is still growing, the decline in GDP per person is a concerning sign. This occurs when population growth outpaces economic growth, which can negatively affect living standards.

Households are also saving less, suggesting that many are relying on savings to manage rising costs. If GDP per person falls again in the June quarter, Australia could enter a per capita recession. This would not mean the entire economy is in recession, but it would indicate that the average Australian is experiencing a decline in their standard of living.

The June quarter will be critical in determining how households respond to higher fuel prices, increased interest rates, and weaker confidence.

Implications for Interest Rates

The Reserve Bank of Australia will meet on June 15–16 to review interest rates. The slow growth, declining GDP per person, and weak discretionary spending all point to the impact of higher interest rates on the economy. At the same time, the central bank must remain vigilant about inflation risks, as fuel prices have risen sharply, and construction prices are still increasing.

The Reserve Bank’s own forecasts suggest that headline inflation is likely to peak in the June quarter. However, the Treasury’s May federal budget forecasted inflation to peak at around 5%. If the conflict in the Middle East ends soon, inflation is expected to return to the Reserve Bank’s target range of 2–3% by next year. However, if the war continues, inflation could rise significantly.

This week’s wage rise for low-paid workers, along with the latest inflation data and unemployment figures, will all be considered by the Reserve Bank board. As Reserve Bank board member Ian Harper noted, making an interest rate decision is always challenging, as it affects every individual in the economy.

On balance, the recent GDP data strengthens the case for the Reserve Bank to hold rates in June and wait for further evidence before deciding on potential increases in August. The central bank now faces an even greater challenge: bringing inflation under control without pushing an already slowing economy into a deeper downturn.